by Craig Love, on September 08, 2023

Kensington Market Insights - August 10th

Market Insights is a weekly piece in which Kensington’s Portfolio Management team will share interesting and thought-provoking charts that we believe provide insight into markets and the current investment landscape.

A House of Cards

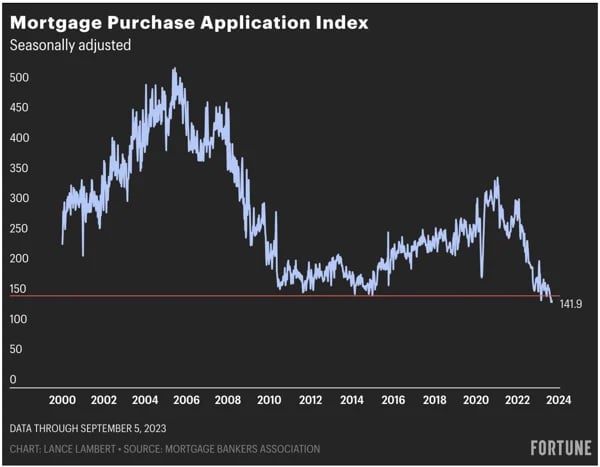

There's a stalemate in the housing sector that is coming to a head and could have far-reaching market implications if it's not resolved. Earlier this week, the US Mortgage Bankers Association announced that Mortgage Purchase Applications (below) have dropped to a 28-year low as mortgage rates hover around 22-year highs.

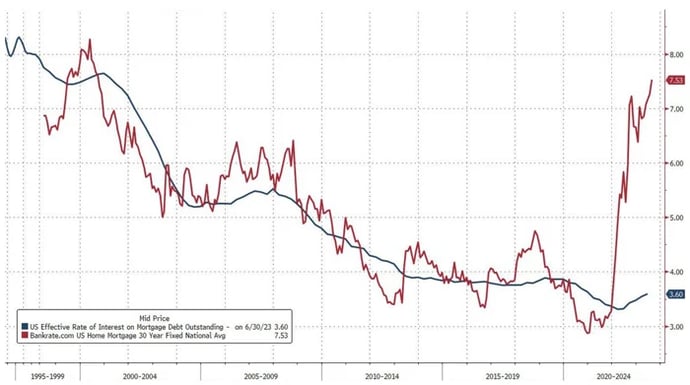

The normal reaction to a drop in demand would be a drop in prices, yet the National Association of Realtors (NAR) announced that the average home price in July was $406,700, a 1.9% increase from a year prior. The issue, of course, is that the drop in demand is being accompanied by a drop in supply. With the average mortgage rate at 7.53% and the average effective rate of existing loans at 3.6% (below), homeowners simply are not selling as they do not want to give up their below-market mortgages and replace them with mortgages at higher prevailing rates.

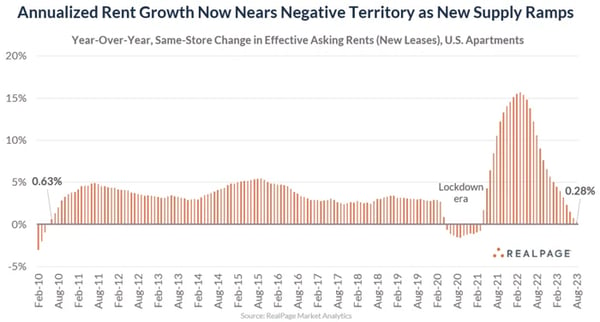

The rental market is providing some relief to potential buyers priced out of homeownership. With apartment construction at a 40+ year high, average rent growth has moved down swiftly in recent months (just 0.28% in August) and is likely to turn negative in the coming months.

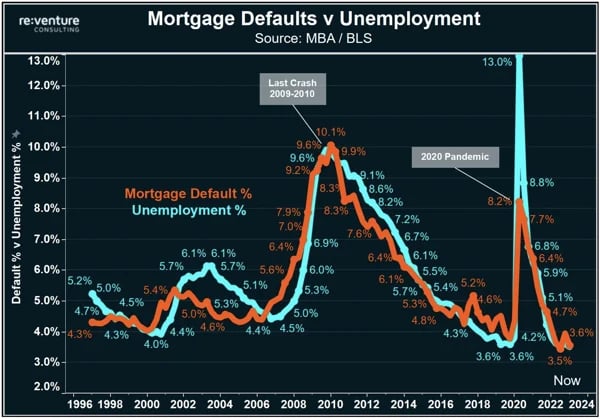

While the rental market can provide temporary relief, something will ultimately need to give in housing, and that something might be a rise in mortgage defaults. There is a near-perfect correlation between mortgage defaults and unemployment (below). The Federal Reserve’s policy of combatting inflation by pushing rates higher is finally beginning to have an impact on the labor market. In August, the unemployment rate increased to 3.8% from 3.5% a month prior. Should the unemployment rate rise above 4% and toward 5%, mortgage defaults are likely to follow.

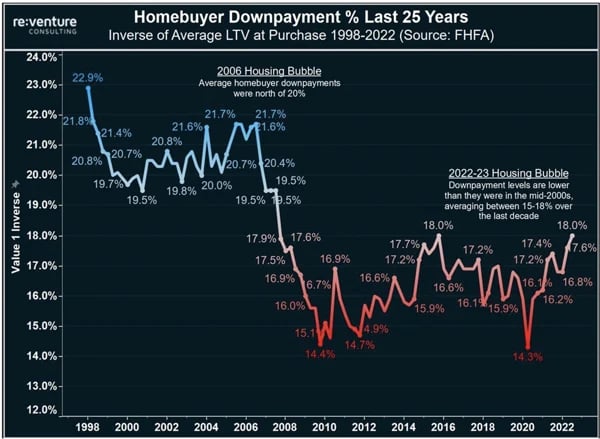

One item exacerbating this concern relates to down payment trends. In recent years, homebuyers have been putting down far less upfront than even in the 2008 era (below). The average down payment was 14% in 2020 and is now 18%, well below the 22%+ seen in the years leading up to 2008. If prices can’t hold, the buffer for homeowners against negative equity is slim and could result in a wave of defaults.

As the 2008 Financial Crisis so clearly illustrated, a housing crisis could be far-reaching in its impact on the overall economy. An added concern is already increasing defaults in corporate loans, credit cards, and auto loans, together suggesting that a threatening credit event may be forthcoming in the months ahead. Credit stress is often a serious threat to markets, but can also lead to meaningful opportunities for those nimble enough to navigate the changing landscape. As always, a tactical approach to markets may be necessary if matters continue to trend toward disruption.

Forward-looking statements are based on management’s then current views and assumptions and, as a result, are subject to certain risks and uncertainties that could cause actual results to differ materially from those projected. This market insight is for informational purposes only and should not be construed as a solicitation to buy or sell, or to invest in any investment product or strategy. Investing involves risk including loss of principal.